Homeowners Insurance 101 (Home Shopping 4/6)

Learn the basics of homeowners insurance and how it protects your home and personal property. Find out what’s covered, how much you need, and tips for saving money on premiums.

Homeowners Insurance 101 | Home Shopping 4/6: Protecting Your New Home

Buying a new home is an exciting milestone, but it also comes with important responsibilities—one of the most crucial being homeowners insurance. Whether you’re a first-time homebuyer or upgrading to a new property, homeowners insurance provides the peace of mind you need to protect your investment. In this Home Shopping 4/6 guide, we’ll walk you through the basics of homeowners insurance, explain its importance, and help you understand what’s covered so you can make an informed decision.

What is Homeowners Insurance?

Homeowners insurance is a type of property insurance that protects your home and personal belongings from damage or loss due to events like fire, theft, vandalism, and certain natural disasters. It also provides liability coverage in case someone is injured on your property. In many cases, mortgage lenders will require homeowners insurance to protect their financial interest in your property.

While each policy can differ slightly, a standard homeowners insurance policy typically includes four main types of coverage:

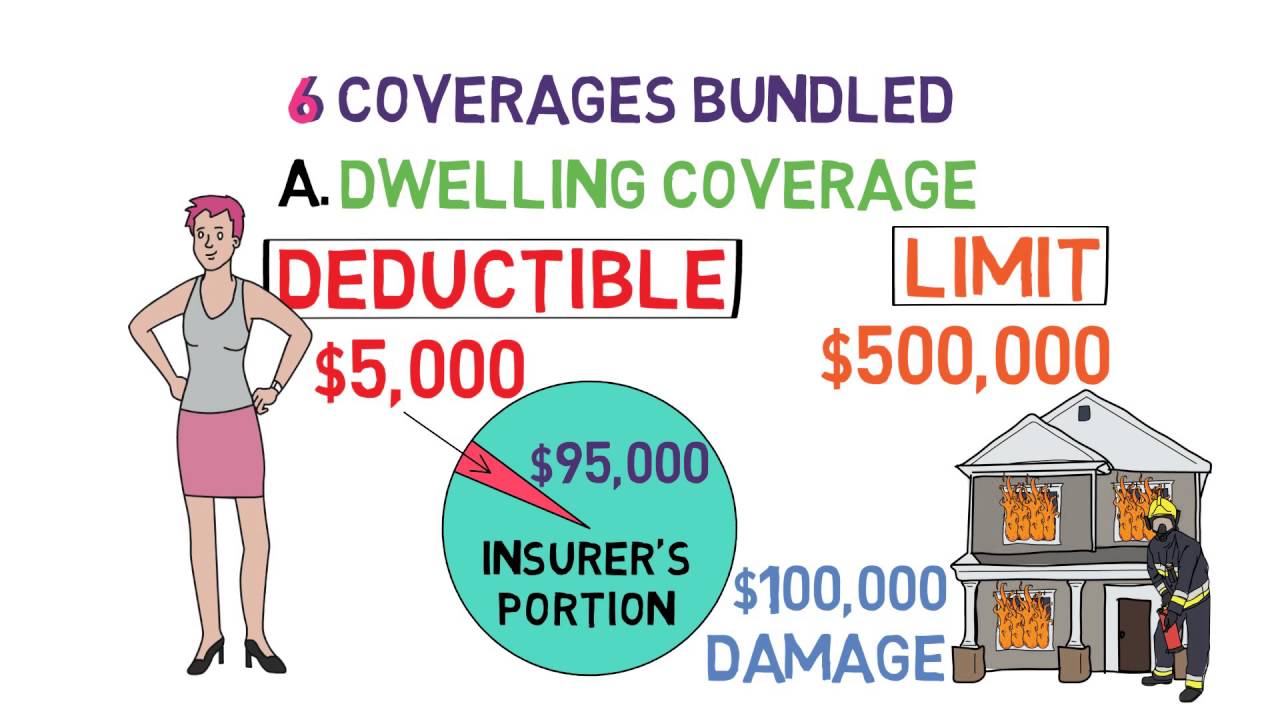

- Dwelling Coverage: Covers the structure of your home, including walls, roof, and foundation, in the event of damage.

- Personal Property Coverage: Protects your personal belongings such as furniture, electronics, and clothing from damage or theft.

- Liability Coverage: Covers medical and legal expenses if someone is injured on your property or if you accidentally damage someone else’s property.

- Additional Living Expenses (ALE): Covers extra living costs if your home is rendered uninhabitable due to a covered loss (e.g., staying in a hotel while repairs are made).

Why Do You Need Homeowners Insurance?

While homeowners insurance is not legally required in most states, if you have a mortgage, your lender will typically require you to carry it. Even if you own your home outright, having homeowners insurance is still a smart decision for several reasons:

- Protects Your Investment: Your home is one of the largest investments you’ll ever make. Insurance helps protect it from unexpected events like fires, storms, or theft, ensuring you don’t bear the full cost of repairs or replacements.

- Covers Liability: If someone is injured on your property, you could be held responsible. Liability coverage ensures you’re not financially devastated by a lawsuit or medical bills.

- Peace of Mind: Knowing that your home and belongings are protected provides peace of mind, reducing stress and worry about the “what-ifs.”

What Does Homeowners Insurance Cover?

Homeowners insurance covers a range of incidents that may damage or destroy your property. While coverage can vary by policy and insurer, common perils covered typically include:

- Fire and Smoke Damage: Coverage for any damage caused by fire or smoke, including repairing your home and replacing damaged personal property.

- Theft or Vandalism: If burglars break into your home or your property is damaged by vandals, your homeowners insurance may cover the loss of personal items and repairs to your home.

- Weather-related Damage: Many policies cover damage from natural disasters like hail, lightning, windstorms, and snow. However, note that certain disasters like floods or earthquakes may require additional coverage.

- Water Damage: Homeowners insurance generally covers damage from burst pipes or plumbing issues, but flooding caused by heavy rains typically requires separate flood insurance.

- Personal Liability: If someone is injured on your property, liability coverage helps with medical bills and legal fees if you are sued.

- Additional Living Expenses: If your home becomes uninhabitable due to a covered disaster, your policy will help with temporary housing costs, such as hotel stays and meals.

What Isn’t Covered by Homeowners Insurance?

While homeowners insurance covers many events, it doesn’t cover everything. Here are a few common exclusions that you should be aware of:

- Flooding: Damage from flooding isn’t typically covered under standard homeowners insurance. If you live in a flood-prone area, consider purchasing a separate flood insurance policy.

- Earthquakes: Most homeowners policies don’t cover earthquake damage. If you live in an earthquake-prone region, you may need additional coverage for this risk.

- Negligence: Damage resulting from neglect or lack of proper maintenance (e.g., mold, rust, or pest infestations) isn’t typically covered.

- High-Value Items: Expensive items like jewelry, art, or collectibles may require separate endorsements or riders to ensure they are fully covered.

How Much Homeowners Insurance Do You Need?

The amount of homeowners insurance you need depends on several factors, including the value of your home, the cost to rebuild, and the value of your personal property. When determining how much coverage to get, consider these key points:

- Dwelling Coverage: Ensure that the policy covers the full cost of rebuilding your home if it were to be destroyed. The cost to rebuild may differ from the market value of your home, so work with your insurance agent to get an accurate estimate.

- Personal Property Coverage: Make an inventory of your personal belongings and estimate their value to determine how much coverage you need for your possessions.

- Liability Coverage: Consider how much liability coverage you’ll need based on your lifestyle and assets. If you frequently host guests or have a pool, higher liability limits may be advisable.

- Additional Living Expenses: You’ll want enough ALE coverage to cover the cost of living in a temporary home for a reasonable amount of time while your home is being repaired.

How to Lower Homeowners Insurance Premiums

While homeowners insurance is necessary, there are several ways to reduce the amount you pay each year:

- Shop Around: Get quotes from multiple insurers and compare prices for similar coverage.

- Increase Your Deductible: A higher deductible often leads to lower premiums. Just make sure you can afford the deductible in case of a claim.

- Bundle Your Insurance: If you have other insurance policies (e.g., auto insurance), consider bundling them with the same insurer for discounts.

- Improve Home Security: Installing security systems, smoke detectors, and deadbolt locks can lower your risk and lead to discounts.

- Maintain Your Home: Regular home maintenance, such as repairing roof leaks or replacing old wiring, can reduce the risk of damage and potentially lower your premiums.

Conclusion: Protect Your Home with the Right Coverage

Homeowners insurance is an essential part of homeownership, offering crucial protection against damage, theft, and liability risks. Understanding the basics of homeowners insurance and knowing what’s covered—and what’s not—can help you make an informed decision when purchasing a policy. As you continue your home-buying journey, make sure to assess your insurance needs and work with a reliable agent to find the best coverage for your new home.

Next Steps: Now that you have a better understanding of homeowners insurance, make sure to review your policy options carefully and shop around to find the best deal. As you move forward with your home shopping process, don’t forget to consider the insurance coverage that best fits your needs!

What's Your Reaction?